The capitalization rate (often referred to as the cap rate) is a key metric used in real estate investing to evaluate the potential return on an investment property. It represents the ratio between the net operating income (NOI) of the property and its current market value or acquisition cost.

Cap Rate Formula:

Cap Rate=Net Operating Income (NOI)Property Value (or Purchase Price)×100\text{Cap Rate} = \frac{\text{Net Operating Income (NOI)}}{\text{Property Value (or Purchase Price)}} \times 100Cap Rate=Property Value (or Purchase Price)Net Operating Income (NOI)×100Where:

- Net Operating Income (NOI): The total income generated by the property (such as rental income) minus operating expenses (like maintenance, property taxes, insurance, and management fees). It does not include financing costs (like mortgage interest) or tax payments.

- Property Value (or Purchase Price): The market value of the property or the price paid to acquire it.

Example:

Suppose you buy a rental property for $500,000, and the property generates $40,000 in annual net operating income. The cap rate would be calculated as follows:

Cap Rate=40,000500,000×100=8%\text{Cap Rate} = \frac{40,000}{500,000} \times 100 = 8\%Cap Rate=500,00040,000×100=8%This means that the property is yielding an 8% return on its value each year, assuming no changes in income or expenses.

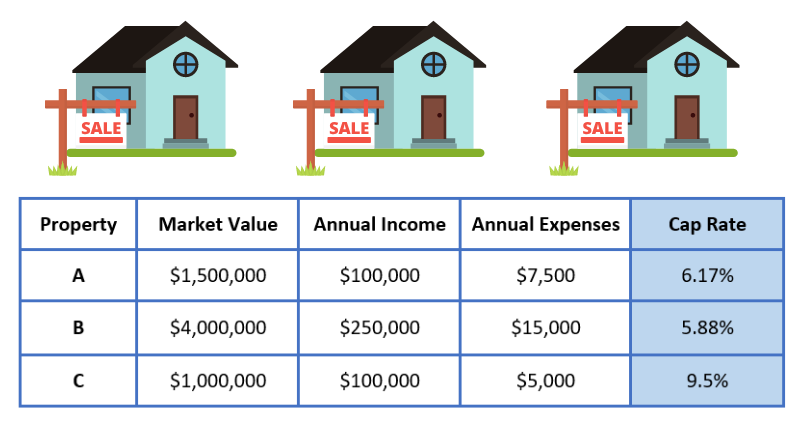

Here is 3 examples of different Cap Rates when taking into account annual expenses:

Key Points to Understand About Cap Rate:

- Risk Assessment:

- Generally, a higher cap rate suggests a higher potential return, but also a higher risk. This could be due to the location of the property, the type of property, or its condition.

- A lower cap rate indicates a lower return, but it is often associated with a lower-risk investment, such as properties in prime locations or those with long-term tenants.

- Market Comparisons: Cap rates allow investors to compare different properties and their expected returns, but they should also consider the local real estate market. A “good” cap rate can vary widely depending on the location, type of property, and the investor’s risk tolerance.

- Estimating Future Returns: The cap rate is often used as a quick way to assess how long it would take to recover the cost of the property (ignoring financing) if the income remains steady. For instance, if the cap rate is 8%, the investor can expect to earn back their investment in about 12.5 years (1 ÷ 0.08 = 12.5 years).

- Impact of Financing: The cap rate is independent of how the property is financed (i.e., whether you pay in full with cash or take out a mortgage). However, the financing method will affect the actual cash-on-cash return you experience, which is a different metric.

- Not a Complete Metric: While useful, the cap rate doesn’t account for factors like future property appreciation, tax benefits, changes in income, or financing costs. It’s primarily a way to evaluate current potential.

Typical Cap Rate Ranges:

- High Cap Rates (8% – 12% or higher): These are often found in less stable, riskier markets or properties that may need repairs, have less desirable locations, or have higher tenant turnover.

- Moderate Cap Rates (5% – 8%): These are typically found in stable markets with moderate risk, such as suburban areas or small cities.

- Low Cap Rates (3% – 5%): These usually reflect high-demand areas, prime locations (e.g., central business districts, luxury properties), or very secure investments.

Limitations of Cap Rate:

- Doesn’t Account for Financing: It doesn’t consider the cost of borrowing, which is important if you’re financing the property.

- Doesn’t Consider Future Growth: It doesn’t take into account potential appreciation in property value, which could be a key factor for long-term investors.

- Assumes Stable Income: It assumes that the property’s income will remain constant, which may not always be the case (e.g., rent increases or decreases, vacancies).

Cap Rate Calculator: https://landlordgurus.com/cap-rate-calculator/

In summary, the cap rate is a handy tool for quickly assessing the return on a real estate investment based on current income, but investors should consider additional factors like financing, property appreciation, and market conditions before making a decision.